May 21, 2026

India’s Gold Loan Market: Growth, Regional Imbalances & Structural Shifts

Market Overview & Explosive Growth:

Gold loans have emerged as the fastest-growing segment in India’s retail lending ecosystem.

-

Surging Growth Rates: The gold loan portfolio has witnessed an explosive growth of 50.4% year-on-year and 15% quarter-on-quarter as of March 2026.

-

Market Size: The total outstanding gold loan market (combining commercial banks and NBFCs) stands at a massive ₹18.62,800 crore (approx. ₹18.6 lakh crore).

-

Retail Ranking: Gold loans have officially become the second-largest product in retail lending, trailing only behind home loans, emphasizing their growing relevance in consumer credit portfolios.

-

Primary Drivers: The surge is primarily driven by skyrocketing global and domestic gold prices (which increase collateral value), rising credit demand, and a growing consumer preference for secured borrowing over high-interest unsecured personal loans.

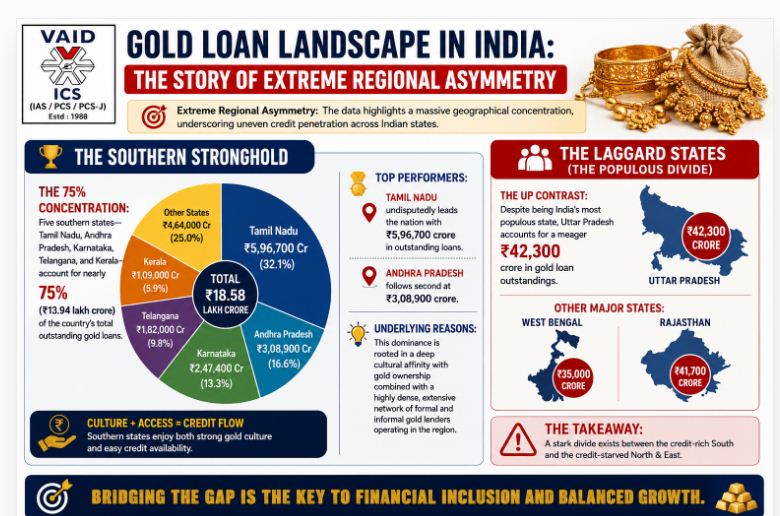

Extreme Regional Asymmetry:

The data highlights a massive geographical concentration, underscoring uneven credit penetration across Indian states.

The Southern Stronghold:

-

The 75% Concentration: Five southern states—Tamil Nadu, Andhra Pradesh, Karnataka, Telangana, and Kerala—account for nearly 75% (₹13.94 lakh crore) of the country’s total outstanding gold loans.

-

Top Performers: * Tamil Nadu undisputedly leads the nation with ₹5,96,700 crore in outstanding loans.

-

Andhra Pradesh follows second at ₹3,08,900 crore.

-

-

Underlying Reasons: This dominance is rooted in a deep cultural affinity with gold ownership combined with a highly dense, extensive network of formal and informal gold lenders operating in the region.

The Laggard States (The Populous Divide):

-

The UP Contrast: Despite being India’s most populous state, Uttar Pradesh accounts for a meager ₹42,300 crore in gold loan outstandings.

-

Other Major States: West Bengal stands at ₹35,000 crore, while Rajasthan accounts for ₹41,700 crore.

-

Economic Takeaway: Densely populated and economically significant states in northern and eastern India still lag heavily behind the South in adopting gold-backed formal borrowing, signaling a massive untapped market.

Market Share & Lender Dynamics:

The report reveals a highly competitive tug-of-war between Public Sector Undertaking (PSU) banks and Non-Banking Financial Companies (NBFCs).

Key Structural Trends & Asset Quality:

-

The Reclassification Impact: Part of the sharp rise in retail gold loans is attributed to the regulatory reclassification of certain agri-gold loans into the retail lending category.

-

Shift to Higher Ticket Sizes: Higher gold prices have naturally prompted borrowers to seek larger loan amounts against their existing gold holdings, leading to more income-generating end-uses rather than just distress consumption.

-

Improving Asset Quality: The segment has shown highly robust credit quality. Early-stage delinquency rates declined across almost all ticket sizes between March 2025 and March 2026, making it a safe, high-quality asset class for financial institutions amidst tightening central bank norms for unsecured retail credit.

भारत का गोल्ड लोन मार्केट: विकास, क्षेत्रीय असमानता और संरचनात्मक बदलाव

बाजार का अवलोकन और अभूतपूर्व वृद्धि:

भारतीय रिटेल लेंडिंग (खुदरा ऋण) इकोसिस्टम में गोल्ड लोन सबसे तेजी से बढ़ने वाले क्षेत्र के रूप में उभरा है।

-

तेज विकास दर: मार्च 2026 तक भारत का गोल्ड लोन पोर्टफोलियो 50.4% सालाना (YoY) और 15% तिमाही-दर-तिमाही (QoQ) की विस्फोटक दर से बढ़ा है।

-

बाजार का कुल आकार: कमर्शियल बैंकों और एनबीएफसी (NBFCs) को मिलाकर देश का कुल बकाया (Outstanding) गोल्ड लोन मार्केट ₹18,62,800 करोड़ (लगभग ₹18.6 लाख करोड़) के विशाल स्तर पर पहुंच गया है।

-

रिटेल सेक्टर में रैंकिंग: होम लोन के बाद गोल्ड लोन आधिकारिक तौर पर खुदरा ऋण का दूसरा सबसे बड़ा उत्पाद बन गया है, जो उपभोक्ता क्रेडिट पोर्टफोलियो में इसकी बढ़ती अहमियत को दिखाता है।

-

विकास के मुख्य कारक: सोने की बढ़ती वैश्विक और घरेलू कीमतें (जिससे गिरवी रखे सोने की वैल्यू बढ़ती है), कर्ज की बढ़ती मांग और असुरक्षित पर्सनल लोन के मुकाबले सुरक्षित लोन के प्रति उपभोक्ताओं का बढ़ता झुकाव इस तेजी की मुख्य वजह हैं।

अत्यधिक क्षेत्रीय असमानता:

इस रिपोर्ट के आंकड़े भौगोलिक रूप से कर्ज की पहुंच में एक बड़े असंतुलन को दर्शाते हैं।

दक्षिण भारत का दबदबा:

-

75% की हिस्सेदारी: देश के पांच दक्षिणी राज्य—तमिलनाडु, आंध्र प्रदेश, कर्नाटक, तेलंगाना और केरल—मिलकर देश के कुल गोल्ड लोन का लगभग 75% (₹13.94 लाख करोड़) हिस्सा रखते हैं।

-

शीर्ष प्रदर्शन करने वाले राज्य: * तमिलनाडु ₹5,96,700 करोड़ के बकाया लोन के साथ पूरे देश में सबसे आगे है।

-

आंध्र प्रदेश ₹3,08,900 करोड़ के साथ दूसरे स्थान पर है।

-

-

मुख्य कारण: दक्षिण भारत में सोने के स्वामित्व (Gold Ownership) के प्रति गहरा सांस्कृतिक लगाव और वहां औपचारिक व अनौपचारिक स्वर्ण ऋणदाताओं (Lenders) का एक बहुत बड़ा नेटवर्क होना है।

उत्तर और पूर्वी राज्यों की स्थिति (आबादी बनाम भागीदारी):

-

उत्तर प्रदेश का विरोधाभास: देश की सबसे अधिक आबादी वाला राज्य होने के बावजूद, उत्तर प्रदेश का कुल बकाया गोल्ड लोन केवल ₹42,300 करोड़ है।

-

अन्य बड़े राज्य: राजस्थान का गोल्ड लोन ₹41,700 करोड़ और पश्चिम बंगाल का ₹35,000 करोड़ है।

-

आर्थिक निष्कर्ष: उत्तर और पूर्वी भारत के घनी आबादी वाले और आर्थिक रूप से महत्वपूर्ण राज्य औपचारिक स्वर्ण ऋण अपनाने में दक्षिण से काफी पीछे हैं, जो यह दर्शाता है कि इन राज्यों में अभी भी विकास की अपार संभावनाएं (Untapped Market) मौजूद हैं।

-

प्रमुख संरचनात्मक प्रवृत्तियां और एसेट क्वालिटी:

-

रीक्लासिफिकेशन (पुनः वर्गीकरण) का असर: रिटेल गोल्ड लोन में इस तेज बढ़ोतरी का एक कारण कुछ कृषि-गोल्ड लोन (Agri-Gold Loans) को नियामक द्वारा खुदरा श्रेणी (Retail Category) में पुनर्वर्गीकृत किया जाना भी है।

-

लोन की राशि में बढ़ोतरी (Higher Ticket Sizes): सोने की ऊंची कीमतों के कारण अब लोग अपने सोने पर ज्यादा कर्ज ले पा रहे हैं, जिससे इस पैसे का इस्तेमाल सिर्फ आपातकालीन खर्चों के बजाय आय-उत्पादक (Income-generating) कार्यों में अधिक हो रहा है।

-

बेहतर एसेट क्वालिटी: इस क्षेत्र में लोन चुकाने का रिकॉर्ड काफी मजबूत रहा है। मार्च 2025 से मार्च 2026 के बीच लगभग सभी श्रेणियों में शुरुआती स्तर की चूक (Early-stage Delinquency) की दरों में गिरावट आई है। केंद्रीय बैंक (RBI) द्वारा असुरक्षित ऋणों पर कड़े होते नियमों के बीच यह वित्तीय संस्थानों के लिए एक सुरक्षित निवेश साबित हो रहा है।

-

May 19, 2026

October 17, 2025

October 16, 2025

October 6, 2025