July 13, 2026

Gist of Daily Articles: 13 JULY 2026 Daily Mains Qn/Model Answer/Mains Concise Note The Hindu/Indian Express

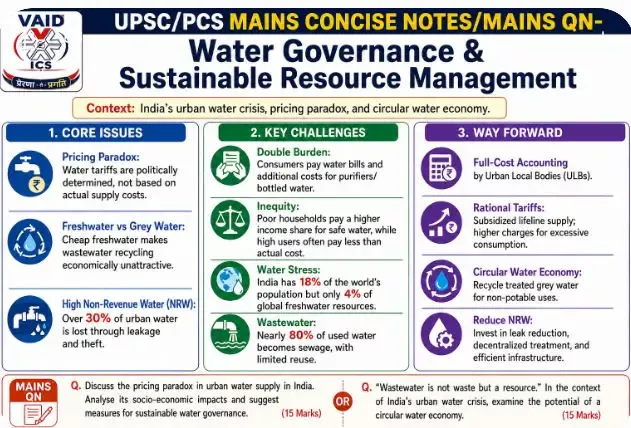

Topic: Water Governance & Sustainable Resource Management

Context: India’s urban water crisis, pricing paradox, and the need for a circular water economy.

1. The Core Problem: The Pricing Paradox:

-

The Disconnect: Urban water tariffs in India are determined by political feasibility rather than the actual cost of abstraction, treatment, storage, and distribution.

-

The “Freshwater vs. Grey Water” Dilemma:

-

Freshwater is priced artificially low.

-

Treating grey water (wastewater from kitchens/baths) costs more than purchasing cheap freshwater.

-

Result: Lack of economic incentive for citizens to invest in grey-water recycling/plumbing.

-

-

The Invisible Cost (Non-Revenue Water – NRW): * In many cities, >30% of supplied water is lost to leakage or theft.

-

Since Urban Local Bodies (ULBs) do not perform “full-cost accounting,” this loss remains invisible, removing the incentive for efficiency.

-

2. Socio-Economic Impacts

-

Double Burden on Consumers: Due to low trust in utility-supplied water quality, households pay twice—once as a (low) water tariff, and again for purchasing/maintaining water purifiers.

-

Inequity (The Justice Aspect): * Lower-income groups either consume unsafe tap water (risking health) or spend a disproportionate share of their income on buying water.

-

Higher-income groups consume substantially more water but often do not pay a proportionate cost.

-

3. Critical Challenges:

-

The Vicious Cycle: Poor service quality leads to low willingness to pay, which restricts revenue for ULBs, leading to further poor service/infrastructure.

-

Resource Scarcity: With 18% of the global population and only 4% of freshwater resources, India is in the highest risk category.

-

Wastewater Management: India turns ~80% of its daily water into sewage. Currently, this is treated as a waste problem rather than a resource opportunity.

4. The Way Forward (Policy Recommendations):

-

Full-Cost Accounting: ULBs must mandatorily publish the full cost of water operations to make “embedded subsidies” visible and accountable.

-

Rational Pricing Model: * Equity: Lifeline quantities per capita should remain subsidized to protect the poor.

-

Progressive Pricing: Higher tariffs for high-volume users to discourage frivolous consumption.

-

-

Circular Urban Water Economy: Treat grey water as an asset. Collect, treat, and price it appropriately for non-potable uses to reduce the burden on freshwater demand.

-

Infrastructure Investment: Shift focus from massive new supply projects to fixing existing leakage (NRW) and decentralized water treatment.

विषय: जल शासन और सतत संसाधन प्रबंधन

संदर्भ: भारत का शहरी जल संकट, मूल्य निर्धारण का विरोधाभास और चक्रीय जल अर्थव्यवस्था (Circular Water Economy) की आवश्यकता।

मूल समस्या: मूल्य निर्धारण का विरोधाभास (Pricing Paradox):

-

राजनीतिक व्यवहार्यता: भारतीय शहरों में जल शुल्क (water tariffs) का निर्धारण वास्तविक लागत (अमूर्तन, उपचार, भंडारण और वितरण) के बजाय राजनीतिक व्यवहार्यता के आधार पर किया जाता है।

-

स्वच्छ जल बनाम ग्रे वॉटर (Grey Water): ताजे पानी की कीमत कृत्रिम रूप से बहुत कम रखी गई है। ग्रे वॉटर (रसोई/स्नान का अपशिष्ट जल) के उपचार की लागत ताजे पानी की कीमत से अधिक है। इसके परिणामस्वरूप, नागरिकों और उद्योगों के पास ग्रे वॉटर पुनर्चक्रण में निवेश करने का कोई आर्थिक प्रोत्साहन नहीं है।

-

अदृश्य लागत (Non-Revenue Water – NRW): कई शहरों में कुल आपूर्ति का 30 प्रतिशत से अधिक पानी रिसाव या चोरी के कारण नष्ट हो जाता है। चूंकि शहरी स्थानीय निकाय (ULBs) ‘पूर्ण-लागत लेखांकन’ (Full-cost accounting) नहीं करते, इसलिए यह बर्बादी खातों में अदृश्य रहती है और इसे सुधारने का कोई प्रोत्साहन नहीं मिलता।

सामाजिक-आर्थिक प्रभाव:

-

दोहरा बोझ: उपयोगिता-आपूर्ति वाले पानी की गुणवत्ता पर भरोसे की कमी के कारण, मध्यम/उच्च वर्ग के लोग दो बार भुगतान करते हैं: एक बार जल शुल्क के रूप में और दूसरी बार वॉटर प्यूरीफायर के रखरखाव पर।

-

असमानता और न्याय: निम्न-आय वर्ग या तो असुरक्षित नल का पानी पीने के लिए मजबूर हैं (स्वास्थ्य जोखिम), या अपनी आय का एक बड़ा हिस्सा पानी खरीदने पर खर्च कर रहे हैं। उच्च-आय वर्ग निम्न-आय समूहों की तुलना में पर्याप्त रूप से अधिक पानी की खपत करते हैं, लेकिन लागत का बोझ समान नहीं है।

प्रमुख चुनौतियाँ:

-

दुष्चक्र (Vicious Cycle): खराब सेवा गुणवत्ता के कारण भुगतान की कम इच्छा → निकाय के पास कम राजस्व → बुनियादी ढांचे में निवेश की कमी → और खराब सेवा गुणवत्ता।

-

संसाधन की कमी: भारत के पास विश्व की 18 प्रतिशत आबादी है, लेकिन केवल 4 प्रतिशत ताजे जल संसाधन उपलब्ध हैं। भारत ‘उच्च जल-जोखिम’ (highest water-risk) श्रेणी में आता है।

-

अपशिष्ट जल का प्रबंधन: भारत अपने दैनिक पानी का लगभग 80 प्रतिशत सीवेज में बदल देता है। इसे अभी भी ‘कचरे’ के रूप में देखा जाता है, न कि एक अवसर के रूप में।

आगे की राह और नीतिगत सुझाव:

-

पूर्ण-लागत लेखांकन (Full-cost Accounting): ULBs को अपनी जल परिचालन की पूरी लागत प्रकाशित करनी चाहिए ताकि निहित सब्सिडी (embedded subsidy) स्पष्ट और जवाबदेह हो सके।

-

तर्कसंगत मूल्य निर्धारण: * समानता: प्रति व्यक्ति जीवन रक्षक मात्रा (Lifeline quantities) पर सब्सिडी जारी रहनी चाहिए।

-

प्रगतिशील मूल्य निर्धारण (Progressive Pricing): अधिक खपत करने वालों के लिए दरें बढ़ाई जानी चाहिए ताकि फिजूलखर्ची पर रोक लगे।

-

-

चक्रीय जल अर्थव्यवस्था: ग्रे वॉटर को एक परिसंपत्ति (Asset) के रूप में माना जाए। इसे अलग से एकत्रित, उपचारित और गैर-पेय उपयोगों के लिए उचित मूल्य पर बेचा जाए, जिससे ताजे पानी की मांग कम हो सके।

-

बुनियादी ढांचे में सुधार: नई आपूर्ति परियोजनाओं के बजाय, रिसाव (NRW) को ठीक करने और विकेंद्रीकृत जल उपचार पर ध्यान केंद्रित करना चाहिए।

May 19, 2026

October 17, 2025

October 16, 2025

October 6, 2025