May 23, 2026

What is the Dividend (Surplus Transfer) to the Government?

Why in the News?

-

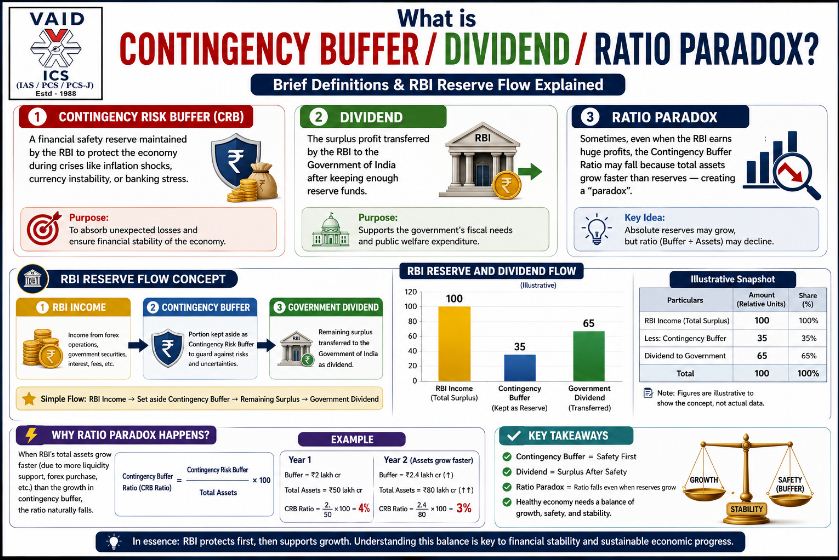

Record RBI Dividend: The Reserve Bank of India (RBI) board has approved a massive surplus transfer (dividend) of ₹2.87 lakh crore to the Government of India for the financial year 2025-26.

-

Growth: This is a 6.7% increase compared to last year’s dividend of ₹2.69 lakh crore.

Key Financial Metrics at a Glance:

Key Points:

1. The Balance Sheet Expansion:

-

RBI’s total balance sheet grew by 20.6% to reach nearly ₹92 lakh crore (as of March 31, 2026).

-

Reasons for Expansion: * Skyrocketing global gold prices.

-

Increased RBI intervention in the bond and foreign exchange (forex) markets.

-

Active liquidity management and a surge in currency in circulation.

-

-

The Ratio Paradox: Even though the RBI transferred 143% more money to its safety net (Contingency Buffer), the actual ratio of the buffer to the balance sheet dropped from 7% to 6.5% simply because the overall balance sheet grew too fast.

2. Shift in Capital Management Strategy:

-

Last Year’s Focus: Strengthening internal safety buffers over distributing surplus money.

-

This Year’s Focus: A calibrated approach—balancing strong internal savings (provisioning) with a larger cash payout to the government.

Fiscal Impact: Why this is Good News for the Government?

The government is facing several financial pressures this year. This mega-dividend acts as a vital financial cushion:

-

Absorbing Rising Subsidies: The extra cash helps the government pay for rising global oil prices, which have spiked the country’s fertilizer and cooking gas subsidy bills.

-

Meeting Budget Targets Easily: * The government’s total target for dividends from the RBI, banks, and financial institutions combined is ₹3,16,000 crore.

-

With RBI alone giving ₹2.87 lakh crore, and SBI/LIC adding over ₹14,000 crore, the government now needs to raise only ₹16,000 crore from all other public banks and institutions to hit its annual target.

-

What is the RBI’s Total Balance Sheet?

Think of the Balance Sheet as a giant ledger that shows the total value of everything the RBI owns (Assets) and everything it owes (Liabilities).

As of March 2026, the RBI’s balance sheet is a staggering ₹92 Lakh Crore.

Why did it grow so big recently?

The RBI doesn’t run a retail shop, but it makes money through huge global assets. Its balance sheet expanded by 20.6% due to:

-

Gold Prices: The RBI keeps massive gold reserves. When gold prices shoot up globally, the value of the RBI’s assets automatically skyrockets.

-

Foreign Forex & Bonds: The RBI buys and sells US Dollars and government bonds to keep the Indian Rupee stable.

-

Currency in Circulation: Every physical note printed in India is technically a liability on the RBI’s balance sheet. As more cash circulates in the economy, the balance sheet grows.

What is the Dividend (Surplus Transfer) to the Government?

Just like a private company shares its profits with its shareholders, the RBI shares its net profits with its sole owner—the Government of India. This profit share is called a Dividend (or Surplus Transfer).

For the financial year 2025-26, the RBI made a massive profit and decided to give ₹2.87 Lakh Crore straight to the government.

How does the RBI earn this profit?

The RBI makes money through:

-

-

Interest earned on foreign assets (like US Government bonds).

-

Interest earned on domestic loans given to Indian banks.

-

Profits made by trading foreign currencies (like buying dollars low and selling high).

-

The “Ratio Paradox” explained simply:

The news mentions that the RBI’s emergency buffer ratio dropped from 7% to 6.5%.

Why? Imagine you have ₹7 saved in a piggy bank when your total worth is ₹100 (a 7% safety net). The next year, you put a lot more money in the piggy bank, making it ₹13. But meanwhile, your total worth jumps to ₹200. Even though you saved more cash, your savings ratio drop to 6.5% of your total worth. That is exactly what happened to the RBI because its balance sheet grew too fast!

Why does this matter to the common man?

The government has to spend a lot of money on public welfare, roads, and subsidies (like keeping cooking gas and fertilizers cheap when global oil prices rise).

Instead of borrowing money from the market or increasing your taxes to cover these costs, the government can now use this ₹2.87 Lakh Crore cash gift from the RBI to pay its bills comfortably.

यहाँ भारतीय रिज़र्व बैंक (RBI) के लाभांश (Dividend), वित्तीय विवरण (Balance Sheet), मुद्रा मुद्रण (Money Printing) और विज़न-लैंग्वेज-एक्शन (VLA) मॉडल से जुड़े सभी महत्वपूर्ण वैचारिक पहलुओं को समाहित करते हुए एक संपूर्ण, समेकित और उच्च स्तरीय फाइनल नोट दिया गया है।

यह मुख्य परीक्षा और त्वरित पुनरीक्षण (Quick Revision) के लिए अत्यधिक उपयोगी है।

भारतीय रिज़र्व बैंक (RBI): वित्तीय प्रबंधन, मौद्रिक नीतियां एवं आधुनिक तकनीक

भाग 1: RBI लाभांश और बैलेंस शीट (नवीनतम घटनाक्रम 2026):

यह चर्चा में क्यों है:

-

ऐतिहासिक लाभांश (Dividend): RBI बोर्ड ने वित्तीय वर्ष 2025-26 के लिए भारत सरकार को ₹2.87 लाख करोड़ के अधिशेष हस्तांतरण (Surplus Transfer/Dividend) को मंजूरी दी है, जो पिछले वर्ष से 6.7% अधिक है।

-

बैलेंस शीट में उछाल: मार्च 2026 तक RBI की कुल बैलेंस शीट 20.6% बढ़कर लगभग ₹92 लाख करोड़ तक पहुंच गई है।

प्रमुख वित्तीय घटक (Metrics):

-

बैलेंस शीट में वृद्धि के कारण: वैश्विक स्तर पर सोने (Gold) की कीमतों में भारी उछाल, विदेशी मुद्रा (Forex) और बॉन्ड बाजार में सक्रिय हस्तक्षेप, तथा बाजार में मुद्रा का प्रवाह (Currency in Circulation) बढ़ना।

-

आकस्मिक जोखिम बफर (Contingency Risk Buffer): RBI ने अपने आपातकालीन सुरक्षा कोष में 143% की भारी वृद्धि करते हुए ₹1.09 लाख करोड़ ट्रांसफर किए।

-

बफर अनुपात विरोधाभास (Ratio Paradox): अधिक नकद बचाने के बावजूद, कुल बैलेंस शीट का आकार बहुत तेजी से बढ़ने के कारण, यह सुरक्षा अनुपात 7% से घटकर 6.5% रह गया।

सरकार पर राजकोषीय प्रभाव (Fiscal Impact):

-

राजकोषीय तकिया (Financial Cushion): यह लाभांश सरकार को बढ़ते वैश्विक तेल संकट के कारण बढ़े उर्वरक और रसोई गैस सब्सिडी बिल को संभालने में मदद करेगा।

-

बजट लक्ष्य की प्राप्ति: सरकार का कुल वित्तीय लक्ष्य ₹3,16,000 करोड़ (RBI + सार्वजनिक बैंकों से) है। इस बड़े लाभांश के बाद सरकार को लक्ष्य पूरा करने के लिए अन्य वित्तीय संस्थानों से मात्र ₹16,000 करोड़ की आवश्यकता होगी।

भाग 2: लाभांश (Dividend) बनाम नया पैसा छापना

अक्सर यह भ्रम होता है कि सरकार को पैसा देने के लिए RBI नई मुद्रा छापता है, लेकिन ये दोनों पूरी तरह भिन्न प्रक्रियाएं हैं:

[ विकल्प A: लाभांश देना (वैध एवं सुरक्षित) ]

RBI की वास्तविक कमाई (ब्याज/विदेशी मुद्रा व्यापार) ──► सरकार को ट्रांसफर ──► बाजार में तरलता स्थिर (नो इन्फ्लेशन)

[ विकल्प B: नई मुद्रा छापना (अवैध एवं विनाशकारी) ]

बिना किसी परिसंपत्ति (Asset) के नोट छापना ──► सीधे सरकार को देना ──► अत्यधिक मुद्रा आपूर्ति ──► अति-मुद्रास्फीति (Hyperinflation)

1. ‘लाभांश’ (Dividend) क्यों कहा जाता है?

-

स्वामित्व का प्रतिफल: कॉर्पोरेट जगत की तरह, चूंकि भारत सरकार RBI की 100% मालिक (शेयरधारक) है, इसलिए RBI अपने वार्षिक शुद्ध लाभ (Net Profit) का जो हिस्सा सरकार के साथ साझा करता है, उसे ‘लाभांश’ या ‘अधिशेष हस्तांतरण’ कहा जाता है। यह वास्तविक और पहले से मौजूद धन होता है, जिससे मुद्रास्फीति (महंगाई) नहीं बढ़ती।

2. सीधे नोट छापकर सरकार को देने का प्रभाव (Direct Monetization):

-

अति-मुद्रास्फीति (Hyperinflation): बाजार में वस्तुओं और सेवाओं का उत्पादन बढ़े बिना यदि नई मुद्रा झोंक दी जाए, तो मुद्रा का मूल्य गिर जाता है (जैसे- जिम्बाब्वे और वेनेजुएला का संकट)।

-

रुपये का अवमूल्यन: वैश्विक बाजार में भारतीय रुपये की साख और कीमत गिर जाएगी, जिससे आयात (जैसे क्रूड ऑयल) अत्यंत महंगा हो जाएगा।

-

विधिक प्रतिबंध: भारत में FRBM अधिनियम, 2003 के तहत RBI द्वारा सरकार के घाटे को पूरा करने के लिए सीधे नोट छापने पर पूर्ण प्रतिबंध है। वर्तमान में RBI केवल अप्रत्यक्ष रूप से (OMOs – ओपन मार्केट ऑपरेशंस के जरिए) बॉन्ड खरीदकर बाजार में तरलता नियंत्रित करता है।

भाग 3: भारत में नोट छापने के मानदंड (Criteria for Printing Money):

RBI अपनी मर्जी से असीमित धन नहीं छाप सकता। इसके लिए एक विधिक और वैज्ञानिक प्रक्रिया अपनाई जाती है:

1. न्यूनतम आरक्षित प्रणाली (Minimum Reserve System – MRS):

-

वर्ष 1956 से भारत में यह प्रणाली लागू है। इसके तहत नई मुद्रा जारी करने के लिए RBI को हमेशा अपने पास कम से कम ₹200 करोड़ का न्यूनतम आरक्षित कोष रखना अनिवार्य है:

-

₹115 करोड़: सोने (Gold) के रूप में।

-

₹85 करोड़: विदेशी मुद्रा या विदेशी प्रतिभूतियों (Foreign Securities) के रूप में।

-

2. मात्रा का निर्धारण करने वाले कारक:

इस न्यूनतम सीमा के ऊपर कितना पैसा छपेगा, इसका निर्धारण निम्नलिखित सांख्यिकीय मानदंडों पर होता है:

-

अनुमानित जीडीपी वृद्धि (Projected GDP Growth): अर्थव्यवस्था के विस्तार के साथ लेनदेन सुगम बनाने के लिए आनुपातिक मुद्रा की आवश्यकता।

-

गंदे नोटों का प्रतिस्थापन (Replacement of Soiled Notes): फटे-पुराने और नष्ट किए गए नोटों के बदले नए नोट छापना।

-

मौसमी मांग (Seasonal Demand): त्योहारों, त्योहारों के सीजन और कृषि कटाई चक्र के दौरान नकदी की बढ़ी हुई मांग।

विशेष तथ्य: ₹10 से लेकर ₹500 या उससे अधिक के बैंक नोट जारी करने का विशेष अधिकार RBI अधिनियम, 1934 के तहत रिज़र्व बैंक के पास है। परंतु, ₹1 का नोट और सभी सिक्के सीधे भारत सरकार (वित्त मंत्रालय) द्वारा ढाले/बनाए जाते हैं, जिन्हें वितरित करने की जिम्मेदारी RBI की होती है।

May 19, 2026

October 17, 2025

October 16, 2025

October 6, 2025