April 22, 2026

Cyber Fraud in India – Trends, Challenges, and Institutional Response

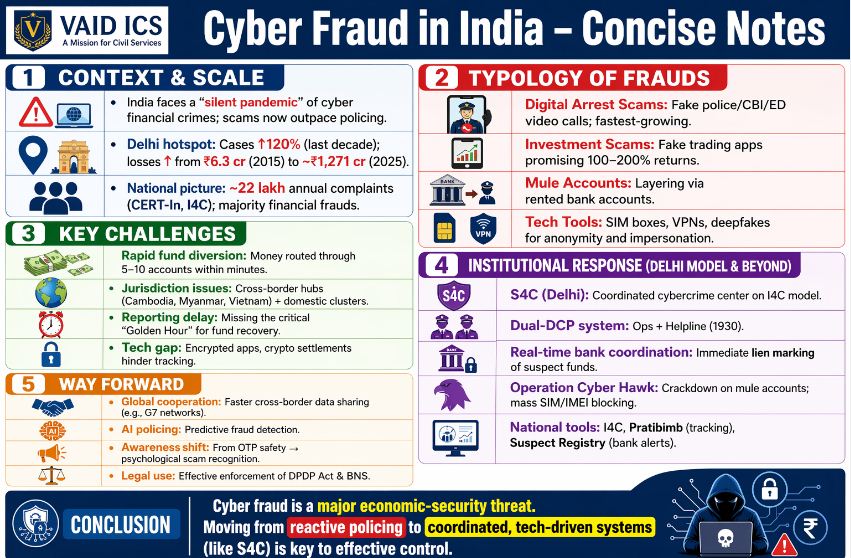

Context & Scale of the Problem:

India is experiencing a “silent pandemic” of cyber financial crimes. As of 2025-26, Delhi has emerged as a major hotspot, reflecting a national trend where the sophistication of scams has outpaced traditional policing.

- Surge in Cases: Delhi witnessed a 120% increase in cyber-related financial frauds over the last decade.

- Financial Impact: Losses in Delhi alone skyrocketed from ₹6.3 crore (2015) to nearly ₹1,271 crore (2025)—a staggering 190-fold jump.

- National Intensity: Data from CERT-In and I4C shows that India now records over 22 lakh cybercrime complaints annually, with financial fraud accounting for the majority.

Typology: What kind of Cyber Frauds?

Modern cybercrimes have shifted from simple phishing to complex psychological and technical operations:

- Digital Arrest Scams: Fraudsters impersonate law enforcement (CBI, ED, Police) via video calls, “arresting” victims virtually to extort money. This is currently the fastest-growing category.

- Investment & Stock Trading Scams: Luring victims through social media groups with promises of 100-200% returns using fake trading apps.

- Mule Account Syndicates: Use of “rented” bank accounts to layer and launder stolen money quickly across borders.

- Technical Exploits: Use of SIM Boxes (to bypass international calling rates and hide location), VPNs, and Deepfakes to create realistic impersonations.

Key Issues and Challenges:

- Multi-layered Money Trails: Scammers move money through 5-10 different bank accounts within minutes, making “hot pursuit” of funds difficult for police.

- Jurisdictional Hurdles: Masterminds often operate from “cyber-safe” havens like Cambodia, Myanmar, and Vietnam (Southeast Asian hubs) or Jamtara/Mewat internally.

- Reporting Lag: The “Golden Hour” (first 2 hours) is critical for freezing funds, but victims often report late due to shock or social stigma.

- Technological Gap: Use of encrypted platforms (Telegram/WhatsApp) and cryptocurrency for final settlements complicates data retrieval.

Recent Initiatives & The Delhi Model (S4C):

The government is moving toward a “Coordinated Enforcement” model:

- State Cyber Crime Coordination Centre (S4C): Delhi Police is establishing S4C on the lines of the National I4C.

- Dual-DCP Structure: One for Operations/Investigation and one for Coordination/Helpline (1930).

- Real-time Banking Linkage: S4C will have dedicated desks to coordinate directly with banks for immediate “Lien Marking” (freezing) of funds.

- Operation ‘Cyber Hawk’: A targeted crackdown on mule account holders and technical infrastructure (blocking 12 lakh+ SIMs and 3 lakh+ IMEIs nationally by 2025).

- Central Platforms: * I4C (Indian Cyber Crime Coordination Centre): The apex body under MHA.

- ‘Pratibimb’ Module: Real-time mapping of cyber-criminal locations.

- Suspect Registry: A shared database of fraudsters’ identifiers used by banks to decline transactions.

Way Forward:

- International Cooperation: Strengthening “Bilateral Cyber Dialogues” and using the G7 24/7 Network for faster cross-border data preservation.

- Technological Upgradation: Adopting AI-driven “Predictive Policing” to identify suspicious transaction patterns before the fraud is reported.

- Financial Literacy: Shifting public awareness from “don’t share OTP” to “identifying psychological manipulation” (e.g., Digital Arrest awareness).

- Legislative Clarity: Ensuring the Digital Personal Data Protection Act (DPDP) and Bharatiya Nyaya Sanhita (BNS) are effectively utilized to prosecute digital-native crimes.

Conclusion:

Cybercrime is no longer just a technical glitch but a threat to economic security and public trust. The shift from “isolated investigation” to “institutional coordination” (as seen in the Delhi S4C initiative) is essential to transition from reactive policing to a proactive, tech-driven defense ecosystem.

May 19, 2026

October 17, 2025

October 16, 2025

October 6, 2025